发现美国制造业复苏的关键

COVID-19 大流行显然以多种方式对制造业构成挑战。随着 2020 年 3 月停工开始压制所有活动,供应链、自动化、工人安全和生产力问题以及更多人员远程工作一跃而起。

现在,随着限制的解除,国家和行业开始向前迈进,制造商有机会将一些经验教训付诸实践。

需要明确的是,过去 18 个月左右的时间不仅仅是坏消息。医疗和其他制造商不惜一切代价开始为卫生保健工作者和其他被认为必不可少的行业的员工生产大量个人防护设备。公司接受了更多的在线培训和销售互动,并推出了增强型网站来与客户互动。一些自动化公司报告称,他们的产品线充足,并且仍然能够在看到自动化项目得到优先考虑的同时完成订单。

那么,美国如何准备在短期内恢复其制造业魔力?价值链中的品牌所有者、OEM 和供应商如何更聪明地前进?部分答案是缓慢而稳定地重建,同时重新思考自动化、通信甚至位置的不可或缺的作用。

大局

新罕布什尔州曼彻斯特 ITR Economics 首席执行官 Brian Beaulieu 表示,在短期内,美国到 2022 年的制造业前景是积极的。

“领先指标非常积极,消费者有很多钱可以支配,”Beaulieu 解释说。 “商业信心正在上升,企业正在经历与刺激相关的流动性激增。”

然而,他警告说,“从大流行衰退的深度出现的增长幅度无法持续到 2022 年。增长速度将放缓。但反映宏观经济制造业的指数将会上升,尽管趋势会出现季节性变化。”

他补充说,显然,ITR 的大流行前预测“主要是基于自然灾害的严重程度”。 “然而,当我们处于大流行的初期——从 3 月 15 日到 3 月 28 日,当时股市正在下跌,州长们正在关闭他们的部分州——我们改变了路线。” ITR 衡量了 2019 年 12 月至 2020 年 2 月八个“头条”类别的数据,在大流行的影响开始充分显现之前,ITR 全面记录了 92.8% 或更高的预测准确度。

对于今年,他继续说道,“由于大流行带来的财政和货币刺激规模之大,我们在许多情况下的预测都需要提高。我们现在似乎走上了正轨,更全面地看到了刺激计划,并能够调整它们可能产生的影响。由于政府行动的中长期后果,刺激措施还使我们重新思考并降低了对本十年中期的期望。”

毫不奇怪,表现最好的是“被指定为必不可少的行业和公司;满足医疗和食品需求的(杂货店等);比其他人预见到关键组件问题;可以灵活地为办公室工作人员提供远程劳动力;提供灵活性和薪酬保障;最近在通过物价上涨的同时提高了工资。”

Beaulieu 对重新构想的供应链的前景感到特别兴奋。 “在岸、就近采购和缩短供应链的趋势非常真实,提供了超越正常商业周期复苏的机会。”

在保护劳动力方面,Beaulieu 指出,“我们看到制造商在可能的情况下提供安全、灵活性和津贴以鼓励劳动力进入设施。”

也就是说,在大流行的大部分时间里,提高自动化“不是问题。正是在大流行的后果和紧张的劳动力市场中,我们看到包括自动化在内的资本支出增加。多年来,ITR Economics 一直主张通过引进新设备来避免劳动力投入的必要性。一些最成功的公司将是那些做到这一点的公司。”这将意味着继续探索和整合人工智能(AI)、加工学习和“越来越能够与人类站在一起”的设备。

回顾和展望

德勤的《2021 年制造业展望》报告在评估疫情对制造业的影响并概述了前进的道路时指出,“制造商力求不受干扰。”

德勤预计 2020-21 年制造业 GDP 年增长率将下降,根据牛津经济模型,预计 2020 年增长率为负 6.3%,2021 年增长率为 3.5%。

此外,报告还指出了全球停工对美国制造业的负面影响,包括:

美国工业生产同比下降 16.5%。

美国工厂总订单同比下降 22.7%。

2020 年 12 月,工业总产能利用率从 4 月的 64.1% 增长至 74.5%,低于疫情前 77% 的水平。

2020 年 12 月,美国工业生产指数为 105.7%,低于大流行前的 110。

“生产和订单水平仍低于 2019 年的水平,”报告指出,“但下降的轨迹已经放缓。”值得注意的是,德勤在总统大选后对 350 多名高管和其他高级领导人进行了调查,其中 63%“对商业前景表现出某种程度或非常积极的看法”。

德勤列举了制造商在推动复苏过程中需要掌握的四个关键方面:

解决预测挑战。报告建议:“2020 年的事件可能是一个警告,需要开发更好的系统来应对中断。”

广泛使用“数字双胞胎”——产品、流程和生产环境的虚拟表示——来模拟它们在现实世界中的表现。

扩大供应选择以减少贸易和其他中断的风险。

“提升”员工的技能,以最大限度地提高员工队伍的灵活性,以应对剧变。

为此,德勤对制造业高管的选举后民意调查发现:

76% 的人打算增加对数字计划的投资,并计划试点和实施更多的工业 4.0 技术。

20% 的人认为管理生产力是他们目前面临的最大挑战。

44% 计划在来年更多地转向区域供应链模式。

31% 的企业计划将部分生产近岸运回美洲。

28% 的人表示,提升技能和培养新技能以适应不断变化的工作环境(尤其是那些强调自动化、数字解决方案和远程工作安排的环境)是最大的挑战。

德勤美国工业产品和建筑行业负责人保罗·韦纳 (Paul Wellener) 表示:“在大流行来袭之前,我们一直在努力保持过去十年建立的势头,但在 2019 年略有下滑。” . “在 2020 年初,情况似乎开始好转——尤其是在某些领域。 ……但展望 2021 年及以后,复苏可能需要更长的时间才能达到大流行前的水平,尤其是在一些……受打击更严重的子行业。”

Wellener 补充说,该行业中一些受灾最严重的部分与商业航空航天、石油和天然气以及其他开采行业以及一些重型设备供应商有关。市场的其他部分“几乎蓬勃发展”——尤其是那些制造家居用品、油漆用品、户外动力设备、健身设备和“与消毒有关的任何产品”的产品。 ……我们喜欢开玩笑说,很多东西已经变成了新的卫生纸。”

他继续说,餐厅、酒店和办公空间对空气过滤系统的需求也激增,“我认为,在我们考虑未来疫苗瓶的运输方式时,我们预计对工业冷冻装置等设备的需求将非常强劲。”

关于数字双胞胎,Wellener 解释了投资它们的一些好处。他指出,从产品开发到工程建设或制造环境,数字双胞胎都可以证明是卓有成效的。对数字孪生能力的投资可以帮助产品更快地推向市场,并有助于了解发电厂或汽车装配线等运营中的“竣工环境”。 “它为您提供了一个很好的机会来了解这些设施是如何组合在一起的,然后您可以以更高效的方式布置它们的内部。”

随着 COVID-19 大流行加剧劳动力短缺和技能差距,Wellener 断言,大流行后劳动力和工作场所的变化将是前所未有的。

“我没有与工业产品或制造公司的 CEO 谈过,他们认为事情会回到 2018 年或 2019 年的样子。每个人都在关注工作的未来是什么样子,在四个围墙内他们的工厂和总部设施的四堵墙内。”他说,所谓的“人才生态系统”将发展到包括更多的贸易组织、社区学院和不同类别的工人,不一定与他们所服务的企业很接近。

与此同时,根据供应管理协会的数据(EPS News 在 1 月 27 日的一篇文章中报道),预计美国制造业增长将持续到今年,并延续去年夏天的势头。具体来说,ISM 预计:

收入净增长 6.9%,在 ISM 追踪的 18 个行业中的 15 个行业实现增长。 ISM 还指出,在接受调查的采购和供应主管中,有 59% 的人预计今年的收入增长。

2.5 制造业岗位增加。

2.7 制造业工资和福利的增加。

2.4 2020 年 CAPEX 投资增加。

一个移动的目标

在大流行期间密切关注赢家和输家是一项艰巨的任务。因此,也将重新评估如何开展业务,因为制造业必然会在供应链管理和整个价值链的沟通等关键领域进行自我改造。

麦肯锡公司位于康涅狄格州斯坦福德的执行合伙人丹·斯旺(Dan Swan)说:“我们在这场大流行中看到,很难概括人们的行为方式。 “这是非常特定于行业的;如果您有一家制造加工产品的公司,他们的工厂经理在制造工厂的大门后面试图阻止供应商卡车在去年春天到达,因为如果供应商的入站材料已经交付,那么他们就拥有它们并且必须支付给他们。”

在其他行业,“情况正好相反,”斯旺继续说道。 “我有一个生产卫生纸的客户,但他们确实无法生产足够的卫生纸。大流行期间发生的事情是一连串的潮起潮落。”在另一个通过家装零售商生产商品的耐用消费品公司的案例中,“他们在 3 月中旬削减了 30% 到 40% 的产量,结果却意识到,当人们有这么多时间在家时,他们把所有的时间都放在了家里。他们在过去 10 年中一直推迟的改进; [公司随后] 将其转回了另一个方向。”

与此同时,斯旺表示拒绝其供应商的加工产品公司现在有“过去 10 年来最大的积压订单”。因此,人们不仅可以说任何一个行业做得好或坏——显然有些行业做得比其他行业好——人们所看到的是前所未有的需求冲击。

最终,他总结道,“领导者可能不应该将每 100 年一次的流行病作为他们的基准,但许多组织意识到他们在供应链中没有他们需要的灵活性。这来自入站材料的可用性;如何扩大或缩小产能;透明地了解您的客户在做什么;以及您的订单是如何下达的。”

需要培育创新

当大流行开始关闭时,对远程工作解决方案的需求立即变得明显。对于传统上在新技术上进展缓慢的公司和行业来说,这是一个粗鲁的觉醒和大规模的行动。并且结果已经结出硕果,这将为大流行之外的制造通信提供信息。

密苏里州切斯特菲尔德市剑桥空气解决方案公司总裁兼卓越制造协会 (AME) 新任董事会主席 Marc Braun 解释说,虽然保证工人安全是第一要务,但这项工作在其他方面也带来了好处。

布劳恩解释说,结果证明是巨大的技术飞跃来自两个关键优先事项:保证工人安全和节省现金以确保满足工资单。对创新和增长的追求是天衣无缝的。

“中小型制造商通常没有人力资源或安全与合规人员来应对过去一年发生的所有监管变化,”布劳恩指出。 “我们开始在我们的网络中创建并依赖我们所谓的公司联盟,在那里我们可以支持我们的整个团队。我们将拥有最好的人力资源领导者,因为所有的人力资源领导者都会聚集在一起,迅速找出这一政策变化,然后将这些政策落实到位。我们的安全和风险缓解人员正在与联盟成员进行持续的社区讨论,他们可以接受这些并迅速整合。我不会称其为技术创新,但这是我们从大流行中获得的永远不会失去的东西。一旦找到它,你就不能放弃它。”

AME 总裁兼首席执行官 Kim Humphrey 是包括造船业在内的多个行业的资深人士,他表示,对制造商系统的冲击有明显的一线希望。

“Organizations that had never allowed their workers to work from home had to totally revamp their technology departments and provide laptops and secure platforms for people to work from home,” she said. “It created this new thing that nobody expected, and a lot of our companies are finding that they’re not going to be sending people back to their workplace. That’s also requiring employees to be much more vocal on best practices.” In a slow-to-change industry like shipbuilding, it “would have taken years to get people to learn how to let people work from home or design from home; they were able to do it in a matter of months.”

Another unplanned benefit emerged as companies beefed up their online presence to include a range of online training, maintenance and virtual tour opportunities.

At Cambridge now, “we have pro audio gear throughout the whole plant to be able to plug our salespeople in like never before,” Braun said. “The whole plant floor is covered by not only wi-fi but pro audio gear capabilities, so you can have a professional mic on multiple people and show the plant floor to our clients.” The impact? Over the past seven months, Cambridge has entertained 2,300 virtual visitors to its plant floor; normal traffic had been 20 to 30 in-person visits a month. “We never thought we’d need audio engineers, but now we’ve got those skills inside and everybody is mic and video capable on the plant floor to showcase what we need to showcase. And that same technology is used for our meetings. Things that would have taken years to create took weeks or days.”

Solutions For Growth

One industry that weathered the storm and offers a lesson for growth is aerospace and defense, explained Eric Chewning, former chief of staff to the Secretary of Defense and a partner in McKinsey’s Advanced Industries Practice.

The defense industry leveraged efficient coordination across supply chains, he noted, and accelerated about $5 billion in government progress payments through to smaller suppliers. Those waivers were granted to keep production sites open, “and the industry itself invested about $10 billion to reconfigure production lines (and) infrastructure for remote working.”

Furthermore, “they had good visibility into what their end-demand requirements were going to be for the most part, because all these programs had their existing schedules. The challenge became how do you stay on schedule? That challenge is something we saw across the board—this lack of multi-tier visibility into the supply chain so you understood the critical areas where you had to provide extra emphasis to make sure that they stayed available. [This happened] particularly in industries that were overly reliant on sole or single-source relationships.”

Going forward, Chewning said, “we’re seeing companies investing in capabilities to realize what’s in their supply chains.” That entails understanding what is in a given supply chain, how visible it is to key stakeholders and knowing what environment your suppliers are working in.

Meanwhile, capital investment to upgrade aging plants and equipment with Industry 4.0 technologies in scale-based manufacturing might require significant spending. In an April 15 article, “Building a more competitive U.S. manufacturing sector,” McKinsey estimated that could require spending $15 billion to $25 billion annually over the next decade—“and capital needs to flow to some 120,000 small and medium-size enterprises.”

With research from McKinsey Global Institute showing a potential $4.6 trillion in trade shifting over the next five years, Chewning stressed four areas where U.S. manufacturers can grasp the competitive edge and capture that value:

Making the right investments in Industry 4.0 productivity tools to fully leverage the benefits of those technologies and processes to enhance productivity.

Ensuring access to capital:“Not just the large guys, but at the small and medium enterprises. The CHIPS act (Creating Helpful Incentives to Produce Semiconductors for America) is a good example, where the government is specifically setting aside $50 million for the semiconductor ecosystem in the U.S.”

Fostering resilient supplier ecosystems:“Leaders realized two things:One, that re-establishment of R&D in manufacturing to drive technical innovation is important. The second is that there are real benefits to co-location with your suppliers and incorporation of those benefits into business cases. Reshoring certain supply-chain activities is increasingly important.”

Developing the manufacturing workforce:“There’s a huge talent dimension to all this. What is the right focus on people development for those Industry 4.0 opportunities, and how do we make sure we’re getting our local ecosystem of trade schools as well as universities providing that type of pipeline as we get people coming back to work?”

Added Swan, “It’s obviously a bit more complicated for some of the smaller manufacturers. One recurring issue we saw in the early days of the pandemic, and then more recently as demand has rebounded in some industries, is that leaders misunderstood their inbound supply chain and where their risks existed.” A case in point:One McKinsey client initially indicated “it had delivered a thorough risk review of its supply chain, and leadership believed they had mitigated their risk. I received a call back a week later from the CPO who explained they were in a bind because they didn’t review any deeper than their Tier 1 suppliers, and now one had confirmed that it sourced a major upstream component from a Tier 2 supplier that was at risk.”

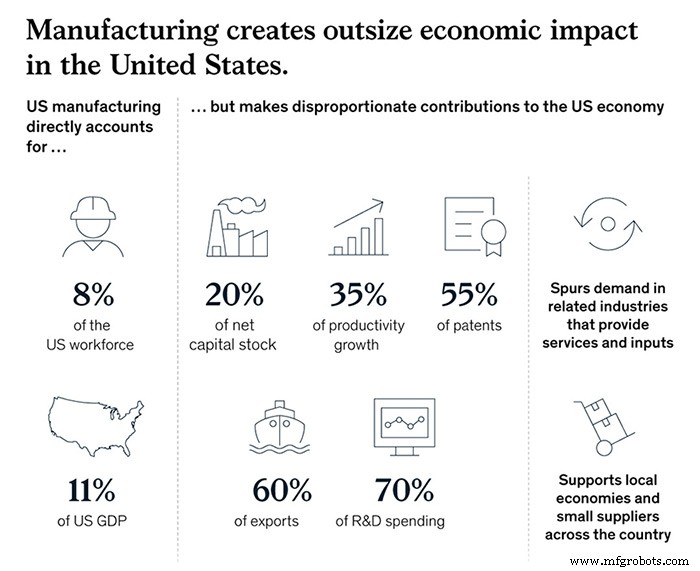

Ultimately, “we’re optimistic” regarding the U.S. manufacturing picture, Chewning asserted. “The current administration and prior administration both made revitalization of the U.S. manufacturing sector a priority, and it’s easy to see why. It’s 8 percent of the workforce, 11 percent of GDP, and it’s responsible for 20 percent of our capital stock, 35 percent of our productivity growth, 55 percent of our patents, 60 percent of exports, and 70 percent of R&D spending. A healthy manufacturing sector creates external benefits to the rest of the economy. Our research has suggested we could boost GDP on the order of $275 billion to $460 billion and add up to 1.5 million more manufacturing jobs by 2030 if we make the right choices.”

Just as vital, Swan added, is “for companies and leaders to think about planning their supply chains for a range of outcomes vs. around the best possible outcome.” Noting that resiliency and flexibility are usually the first casualties of cost-cutting measures, Swan asserted that “there will be a mindset shift required of our leaders to ask what the range of outcomes could be within our supply chain and how we can set ourselves up to be successful.

“This all is top of mind for people across the public and private sectors,” Swan continued. “We need our companies and manufacturing leaders to examine head-on what is it going to take to be successful five years from now, 10 years from now. We need more people to be thinking big and bold about what they need and how they can pull it off. I’m really encouraged by the fact that there are more people thinking that way these days.”

自动化控制系统